2025 review and 2026 outlook: Reflections from Philippe Bekhazi on digital assets' institutional era| AI generated image by XBTO

Every December, I revisit the same question I've asked myself since founding XBTO in 2015: What changed this year that institutional allocators couldn't ignore?

In our early years, the answer was often measured in infrastructure milestones: first regulated Bitcoin futures, first institutional custody solutions, first fiat onramps that didn't feel like navigating a frontier market.

In 2024, the answer was spot ETF approvals.

But 2025? This has been the year those approvals translated into sustained institutional adoption at scale.

Bitcoin reached $126,210 in October. More telling: BlackRock's IBIT surpassed $95 billion AUM in just 435 days, faster than any ETF in history. Regulatory agencies shifted from enforcement to enablement. Stablecoins surpassed $300 billion in market cap and processed $15.6 trillion in quarterly transfers. And tokenization validated blockchain rails for traditional finance, with realworld assets growing 223% to $35.66 billion.

This wasn't retail speculation driving prices. It was institutional capital finding predictable entry points through regulated vehicles, sophisticated infrastructure, and clear regulatory frameworks. After a decade of building toward this moment, 2025 proved that digital assets aren't an allocation risk. They're a portfolio requirement.

2025: The year digital assets became portfolio essentials

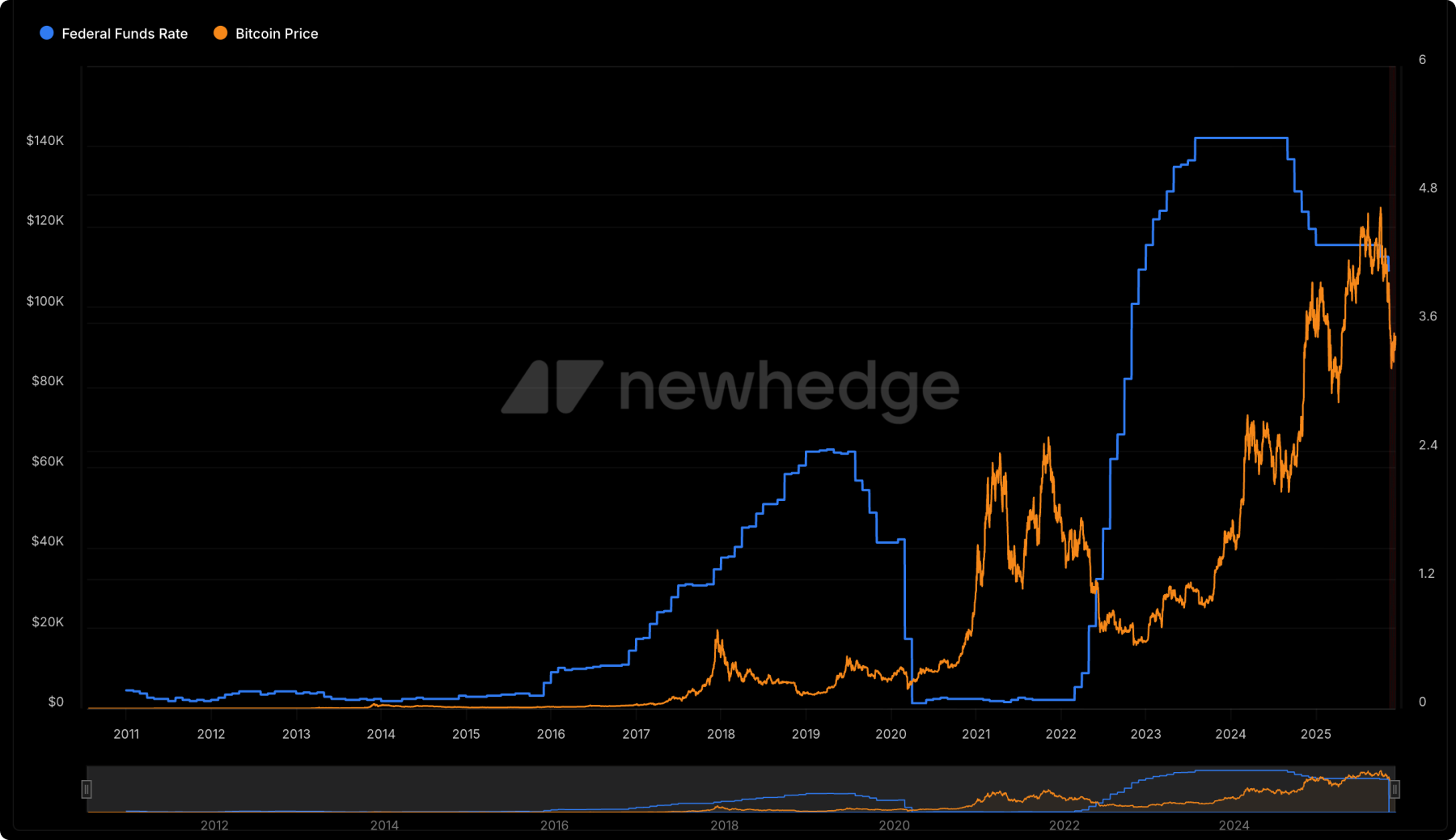

The Federal Reserve delivered three consecutive 25 basis point rate cuts in September, October, and December, bringing the federal funds rate to 3.5%-3.75% and ending quantitative tightening in December.

Lower rates reduced the opportunity cost of non-yielding assets like Bitcoin, while inflation remained elevated (CPI at 3.0%, PCE at 2.7%) but declining, sustaining the inflation hedge narrative without triggering policy reversal.

Gold surged above $4,000/oz (up 60%+ YTD), while Bitcoin rallied to $126,210, reinforcing safe-haven convergence.

Bitcoin vs Federal funds rate

Bitcoin vs. Federal funds rate historically - Major Bitcoin uptrends have emerged as U.S. interest rates declined and monetary conditions eased. Recent rate normalization raises the possibility of renewed upside, though the extent to which this is already priced remains uncertain.

The SEC shifted from enforcement to rulemaking: May clarified staking doesn't constitute securities transactions, September reduced altcoin ETF approval timelines from 12-18 months to 60-90 days, and November IRS guidance allowed ETFs to stake assets without tax penalties. Result: predictable frameworks for custody, compliance, and tax treatment.

U.S. spot Bitcoin ETFs reached $122 billion in total AUM as of December 10, 2025, up from $27 billion at the start of 2024.

BlackRock's IBIT surpassed $95 billion AUM in just 435 days, the fastest ETF to reach this milestone in history, and now holds approximately 800,000 BTC (3.8% of circulating supply). Despite Bitcoin's retracement from its October peak, institutional demand remained resilient, with daily trading volumes averaging ~ $4. billion.

Bitcoin ETF AUM

Ethereum reached $4,953.73 all-time high in August, with spot ETH ETF AUM reaching $17.98 billion by year-end led by BlackRock's ETHA. REX Shares and Osprey launched the first U.S. Ethereum staking ETF in September, enabling 3.95% average staking returns. Solana spot and staking ETFs launched in mid-November 2025, with analysts projecting $3.8-$7.2 billion in institutional inflows as Bloomberg raised approval odds for remaining altcoin ETFs to 95%.

Public companies collectively hold 1,075,000+ BTC, representing 4.8% of Bitcoin's circulating supply, up 40% in Q3 2025 alone. Strategy (formerly MicroStrategy) leads with 660,624 BTC valued at $60.8 billion, raising $10.5 billion in 2025 through at-the-market stock offerings and preferred shares channeled directly into Bitcoin purchases.

Q2 2025 corporate acquisitions (131,000 BTC) outpaced ETF buyers (111,000 BTC) for the third consecutive quarter. Companies announcing Bitcoin treasury strategies experienced average 150% stock price increases within 24 hours (Source: Nasdaq).

Public companies Bitcoin treasuries

Stablecoin market cap grew 47% to $312 billion, with USDT ($185B) and USDC ($78B) controlling 94% of supply. Q3 transfer volumes hit $15.6 trillion (Source: Coinmarketcap), the strongest quarter on record.

Venture capital interest surged as stablecoins transitioned from crypto infrastructure to mainstream payment rails, with institutional adoption accelerating across treasury management and B2B settlement.

Tokenized real-world assets surged 223% to $35.66 billion, led by BlackRock's BUIDL ($2.85B) and Franklin Templeton's BENJI ($776M). U.S. Treasury tokens dominated with $6.2B across 232 issuers and 523,564 holders. But JPMorgan noted RWA "underperforming expectations," with BlackRock BUIDL experiencing $0.6B outflows in May-August.

Volumes increased, infrastructure matured, yet the revolutionary use cases justifying tokenization's promise remain elusive.

Bitcoin retraced 27% from October's $126,210 peak to $90,272 as of December 9. But 30-day realized volatility compressed to 6.46%, lower than historical 50%+ averages, driven by institutional custody concentration (BlackRock + MicroStrategy control ~7% of supply) and derivatives maturity.

The deeper driver: volatility became expensive versus traditional assets, prompting institutions to sell options for income generation (covered calls, put selling), which stabilized markets while capturing premium.

2025 established the foundation: regulatory clarity, institutional infrastructure, macroeconomic support. Digital assets transitioned from emerging allocation option to portfolio requirement. The question for 2026 isn't whether this continues; it's what comes next.

Moving forward: Predictions for 2026

Looking ahead to 2026, the foundation laid in 2025 has created a springboard for what could be a defining year. Building on this momentum, here are some predictions for the year ahead.

After facing headwinds from macro uncertainty and the October 2025 federal government shutdown that paused altcoin ETF approvals, Bitcoin is positioned to regain its footing in 2026. The catalysts: Jerome Powell's potential replacement as Fed Chair in May 2026 and a more accommodative monetary policy environment. With inflation declining but still elevated, the Fed is more likely to continue cutting rates than reversing course.

As Bitcoin matures into an institutional safe haven, macro policy shifts drive capital allocation decisions and institutional infrastructure is positioned to absorb selling pressure during volatility spikes.

Gold's 60%+ return in 2025, its strongest performance since 1979, reinforces its role as the ultimate refuge currency during geopolitical uncertainty and currency debasement concerns. Central bank buying, sovereign wealth diversification, and structural dollar concerns will keep gold elevated in 2026.

While Bitcoin offers "digital gold" characteristics, traditional gold's 5,000-year track record, zero counterparty risk, and recognition by every central bank globally ensure its continued dominance as portfolio ballast.

Institutional allocators don't need to choose between gold and Bitcoin. Gold provides proven stability during systemic stress. Bitcoin offers asymmetric upside and technological superiority for the next generation of treasury management. Portfolios benefit from both.

The premium valuations that Bitcoin treasury companies like Strategy (formerly MicroStrategy) enjoyed in 2025, often trading at 2.5x their Bitcoin net asset value, will compress in 2026. As more public companies adopt Bitcoin treasury strategies (over 200 now hold BTC, up 40% in Q3 2025 alone), the "pioneer premium" erodes.

Market saturation, rising capital costs, and investor scrutiny of leverage ratios will push most digital asset treasury companies (DATCs) to trade at or below their Bitcoin holdings' market value. Only companies demonstrating superior execution, accretive capital raising, operational cash flow generation, or unique structural advantages, will command sustained premiums.

The 150% average stock surge following Bitcoin treasury announcements is unsustainable as adoption becomes commonplace. Investors should focus on companies with differentiated strategies rather than chasing every corporate Bitcoin announcement. Premium compression creates opportunities for selective allocators.

Despite staking ETH ETF launches and Solana ETF approvals, Ethereum and Solana are unlikely to match Bitcoin's performance in 2026. The reason: capital flows into Bitcoin are driven by macro factors - inflation hedging, safe-haven demand, corporate treasury adoption, and institutional portfolio diversification. Flows into non-Bitcoin assets remain largely speculative, driven by narratives around smart contract utility, DeFi growth, or ecosystem development rather than fundamental portfolio allocation decisions. Until Ethereum and Solana establish clear macro narratives comparable to Bitcoin's "digital gold" positioning, their institutional adoption will lag - regardless of infrastructure improvements or regulatory approvals.

The $312 billion stablecoin market ($15.6 trillion Q3 transfer volume) will see dozens of new entrants in 2026 - banks launching proprietary stablecoins, governments exploring CBDCs, and protocols creating yield-bearing variants. Most will fail to gain traction. Network effects are insurmountable: USDT ($185B) and USDC ($78B) control 94% of supply because they're integrated into every exchange, accepted as derivatives collateral, and trusted for cross-border settlement.

New stablecoins face a cold-start problem - liquidity, acceptance, and trust take years to build. Expect proliferation of stablecoins serving niche use cases (loyalty programs, closed-loop payments, regional corridors), but Tether and Circle will continue leading USD-denominated stablecoin infrastructure.

Is deflation among us? The more relevant question for 2026: Is the Fed more likely to cut rates than hold or increase them? The answer is yes. Despite elevated inflation prints in 2025 (CPI at 3.0%, PCE at 2.7%), disinflationary pressures, slowing wage growth, softening consumer demand, and global manufacturing weakness, suggest the Fed's next move is down, not up.

Powell's potential replacement in May 2026 could accelerate dovish policy if the new chair prioritizes growth over inflation control. Further rate cuts reduce opportunity costs for non-yielding assets (Bitcoin, gold) while supporting risk assets (equities, crypto). This creates a favorable environment for digital asset allocations, particularly yield-generating products like Ethereum staking ETFs and DeFi protocols offering real returns.

Zcash (ZEC) and other privacy-focused cryptocurrencies address legitimate concerns, financial privacy, protection from surveillance, and quantum-resistant cryptography. These are important subjects. That said, regulatory pressure, exchange delistings, and institutional aversion to assets perceived as facilitating illicit activity will keep privacy coins marginalized in 2026.

The regulatory environment post-2025 clarity benefits transparent, traceable assets (Bitcoin, Ethereum) while creating existential risks for privacy-preserving protocols. Until privacy coins develop institutional-grade compliance frameworks, selective disclosure, regulated privacy, or tiered transparency, they remain speculative bets rather than portfolio components. The ZEC trade fizzles not because the technology lacks merit, but because regulatory and institutional adoption barriers are insurmountable near-term.

2026 represents an inflection point: the infrastructure is built, regulatory clarity exists, and institutional adoption is accelerating. But not all narratives will be delivered. Bitcoin's macro positioning, gold's refuge status, and established stablecoin dominance offer high-conviction opportunities. Altcoin ETFs, corporate treasury proliferation, and privacy coins face execution risks that require selective positioning.

After a decade building XBTO through multiple cycles, I've learned that institutional success in digital assets comes from distinguishing signal from noise. 2026 will separate speculators from allocators, and hype from fundamental value creation.

The opportunities are real. The discipline required to capture them is even more important.

Collapse

The full breakdown

In our first article, "Navigating Crypto Volatility: The Advantages of Active Management," we explored how the high volatility and low correlation of digital assets with traditional asset classes create unique opportunities for active managers. We discussed how these characteristics enable active managers to execute tactical trading strategies, capitalizing on short-term price movements and market inefficiencies. Building on that foundation, we now turn our attention to the unique market microstructure of digital assets.

Conducive market microstructure of digital assets

The market microstructure of digital assets - a framework that defines how crypto trades are conducted, including order execution, price formation, and market interactions - sets the stage for active management to thrive. This unique ecosystem, characterized by its continuous trading hours, diverse trading venues, and substantial market liquidity, offers several advantages for active management, providing a fertile ground for sophisticated investment strategies.

24/7/365 market access

One of the defining characteristics of digital asset markets is their continuous, round-the-clock operation.

Unlike traditional financial markets that operate within specific hours, cryptocurrency markets are open 24 hours a day, seven days a week, all year round. This continuous trading capability is particularly advantageous for active managers for several reasons:

- Immediate response to market events: Unlike traditional markets that close after regular trading hours, digital asset markets allow managers to react immediately to breaking news or events that could impact asset prices. For instance, if a significant economic policy change occurs over the weekend, managers can adjust their positions in real-time without waiting for markets to open.

- Managing volatility: Continuous trading provides more opportunities to capitalize on price movements and volatility. Active managers can take advantage of this by implementing strategies such as short-term trading or hedging to mitigate risks and lock in gains whenever market conditions change. For instance, if there’s a sudden drop in the price of Bitcoin, managers can quickly sell their holdings to minimize losses or buy in to capitalize on the lower prices.

Variety of trading venues

The proliferation and variety of trading venues is another crucial element of the digital asset market structure. The extensive landscape of over 200 centralized exchanges (CEX) and more than 500 decentralized exchanges (DEX) offers a wide array of platforms for cryptocurrency trading. This diversity is beneficial for active managers in several ways:

- Risk management and diversification: By spreading trades across various exchanges, active managers can mitigate counterparty risk associated with any single platform. Additionally, the ability to trade on both CEX and DEX platforms allows managers to diversify their strategies, incorporating different levels of decentralization, regulatory environments, and security features.

- Arbitrage opportunities: Different venues often exhibit price discrepancies, presenting arbitrage opportunities. For example, managers can buy an asset on one exchange at a lower price and sell it on another where the price is higher, thus generating risk-free profits.

- Access to diverse liquidity pools: Multiple trading venues provide access to diverse liquidity pools, ensuring that managers can execute large trades without significantly impacting the market price.

Spot and derivatives markets (Variety of instruments)

The seamless integration of spot and derivatives markets within the digital asset space presents a considerable advantage for active managers. With substantial liquidity in both markets, they can implement sophisticated trading strategies and manage risk more effectively.

For instance, as of August 8 2024, Bitcoin (BTC) boasts a daily spot trading volume of $40.44 billion and an open interest in futures of $27.75 billion. Additionally, derivatives such as futures, options, and perpetual contracts enable managers to hedge positions, leverage trades, and employ complex strategies that can amplify returns.

Overall, the benefits for active managers include:

- Hedging and risk management: Derivatives offer a powerful tool for hedging against unfavorable price movements, enabling more efficient risk management. For instance, a manager holding a substantial amount of Bitcoin in the spot market can use Bitcoin futures contracts to safeguard against potential price drops, thereby enhancing risk control.

- Access to leverage: Managers can use derivatives to leverage their positions, amplifying potential returns while maintaining control over risk exposure. For instance, by employing options, a manager can gain exposure to an underlying asset with only a fraction of the capital needed for a direct spot purchase, thereby enabling more capital-efficient investment strategies.

- Strategic flexibility: By integrating spot and derivatives markets, managers can implement sophisticated strategies designed to capitalize on diverse market conditions. For instance, they may engage in volatility selling, where options are sold to generate income from market volatility, regardless of price direction. Additionally, managers can leverage favorable funding rates in perpetual futures markets to enhance yield generation. Basis trading, another strategy, involves taking offsetting positions in spot and futures markets to profit from price differentials, enabling returns that are independent of market movements.

Exploiting market inefficiencies

Digital asset markets, being relatively nascent, are less efficient compared to traditional financial markets. These inefficiencies arise from various factors, including regulatory differences, market segmentation, and varying levels of market maturity. For example:

- Pricing anomalies: Phenomena like the "Kimchi premium," where cryptocurrency prices in South Korea trade at a premium compared to other markets, create arbitrage opportunities. Managers can exploit these by buying assets in one market and selling them in another at a higher price.

- Exploiting mispricings: Active managers can identify and capitalize on mispricings caused by market inefficiencies, using strategies such as statistical arbitrage and mean reversion.

The unique aspects of the digital asset market structure create an exceptionally conducive environment for active management. Continuous trading hours and diverse venues provide the flexibility to react quickly to market changes, ensuring timely execution of trades. The availability of both spot and derivatives markets supports a wide range of sophisticated trading strategies, from hedging to leveraging positions. Market inefficiencies and pricing anomalies offer numerous opportunities for generating alpha, making active management particularly effective in the digital asset space. Furthermore, the ability to hedge and manage risk through derivatives, along with exploiting uncorrelated performance, enhances portfolio resilience and stability.

In our next article, we'll delve into the various techniques active managers employ in the digital asset markets, showcasing real-world use cases.

Read full disclaimer