Bitcoin’s IPO moment: From early holders to institutions | AI generated image by XBTO

Bitcoin is undergoing its “Distribution IPO”, a methodical transition where early adopters realize gains and supply is absorbed by permanent institutional balance sheets. This represents more than a narrative shift or graduation ceremony; it is a passing of the torch from concentrated, early-stage risk capital to institutional fiduciaries.

Early 2026 has produced a familiar paradox: traditional risk assets rally while Bitcoin's price lacks directional urgency. Rather than signaling dysfunction, this reflects a transition. The right question is not when does Bitcoin move, but what is Bitcoin becoming.

The answer lies at the intersection of market structure and macro: Bitcoin is shifting from a high-beta proxy into a monetary trust trade.

Act I: The high-beta trap

For years, Bitcoin traded as a liquidity-sensitive, high-beta asset that mapped cleanly onto the Nasdaq during risk-on cycles. That correlation has fractured under a new market regime.

When an asset is in its venture phase, price is driven by marginal sentiment and speculative capital with short horizons. In that regime, correlations to broader risk appetite dominate. Bitcoin has now exited this phase. As XBTO’s CEO, Philippe Bekhazi, discussed in his recent CoinDesk interview, Bitcoin has effectively "had its IPO”, marking the transition into an institutional era in which market outcomes are driven by structural forces rather than retail reflexes.

Framing Bitcoin as a speculative asset is the high-beta trap. From an institutional standpoint, the current market consolidation does not reflect a loss of momentum; it reflects a necessary balance-sheet absorption.

The Guardrail: Our "Digital Gold" thesis would be invalidated by a sustained, positive correlation between Bitcoin and the Nasdaq during a period of high inflation or debt crisis. In such a scenario, Bitcoin would continue to trade as a high-risk technology asset rather than maturing into a monetary instrument.

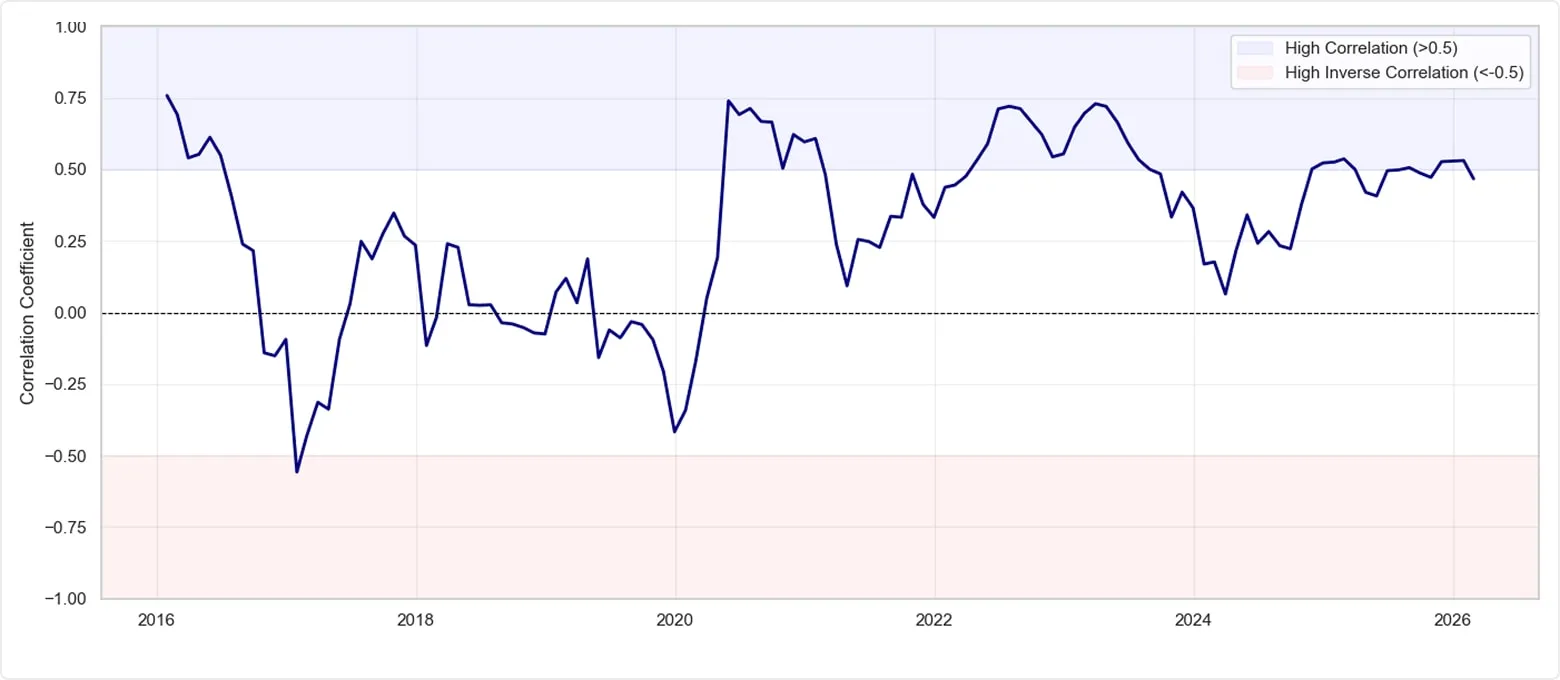

BTC vs Nasdaq 100: 12-month rolling correlation (Monthly data, since 2015)

The 12-month rolling correlation between Bitcoin and Nasdaq illustrates the 'high-beta trap,' specifically highlighting the 2020–2022 period where Bitcoin transitioned into a 'venture phase' and correlation with the Nasdaq surged above 0.70. While the trend has since retreated from those historic highs, supporting the argument that Bitcoin has 'had its IPO' and is exiting the era of pure retail speculation, the persistence of the correlation near 0.50 signals that the transition is still heavily contested. For the 'Digital Gold' thesis to be fully realized, this trendline must structurally decouple and trend lower, confirming that Bitcoin is being valued as a monetary instrument rather than a tech stock.". Source: Data from Yahoo finance.

Act II: The distribution IPO

Bitcoin’s current structure is best understood through its market plumbing. The distribution IPO denotes a large-scale liquidity event in which institutional rails and market depth are now sufficient to absorb large sell-side flows, allowing early holders to exit sizable positions without disorderly price impact.

The passing of the torch

For years, early holders faced a binding structural constraint: substantial unrealized wealth that could not be monetized at scale. In 2015, a nine-figure sale would have overwhelmed available liquidity; and by 2019, even larger exits faced the same limitation. The market simply lacked the depth to absorb concentrated sell-side flows. That constraint has now eased. ETFs provide institutional bid at scale, BlackRock's IBIT alone holds over 750,000 BTC, with assets under management (AUM) exceeding $50 billion. Corporate treasuries hold balance sheet positions, and sovereign wealth funds have entered the allocation conversation. Market depth that once prevented orderly monetization now supports multi-billion-dollar single-client liquidations without significant price action. Early believers who assumed existential risk are finally realizing gains into a market capable of absorbing them.

A clear illustration is Galaxy Digital’s execution of a $9 billion sell-side program for a single client, demonstrating a methodical institutional monetization rather than retail-driven selling.

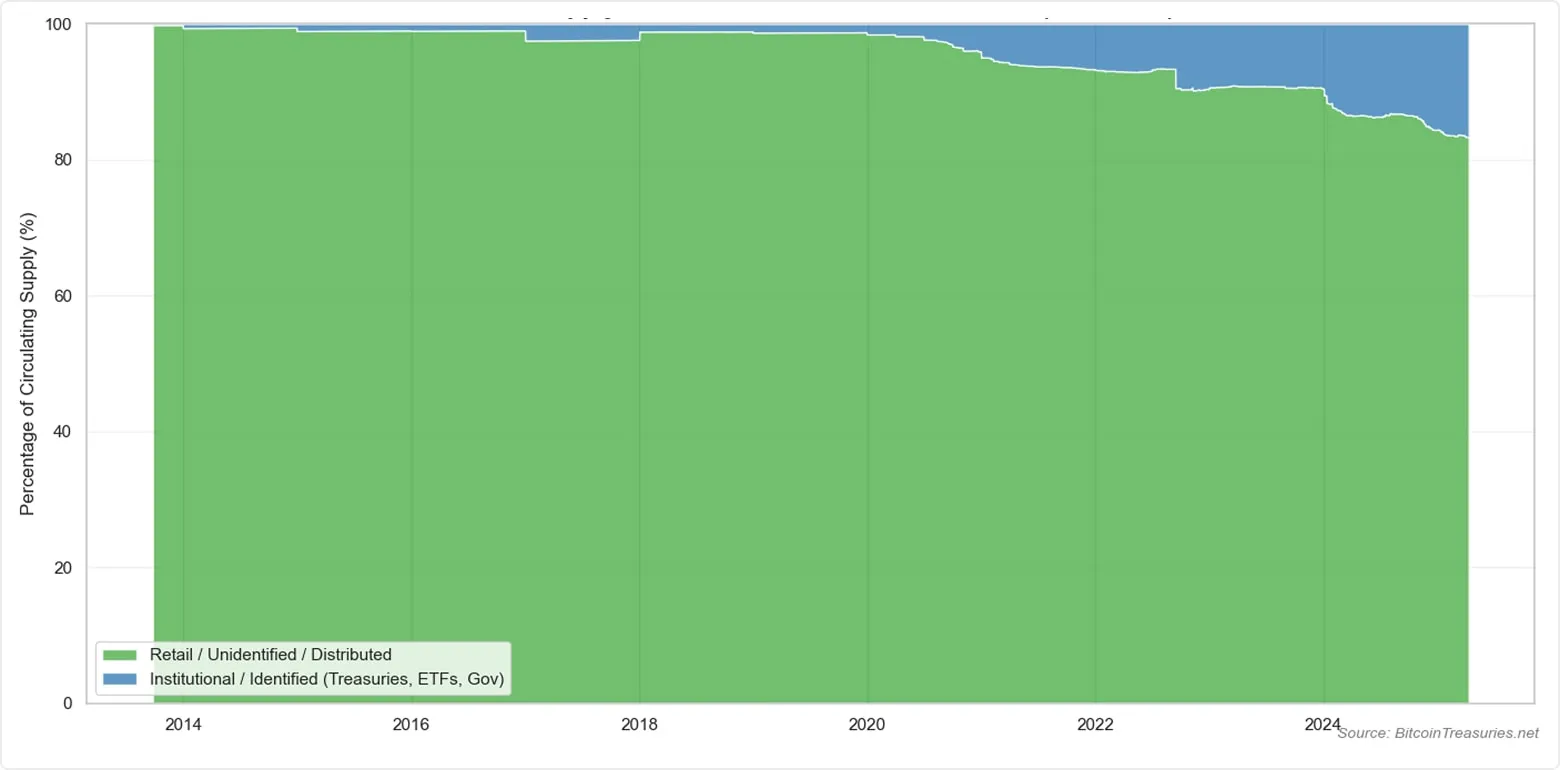

Bitcoin supply distribution: Retail vs. Institutional (Estimated)

Source: BitcoinTreasuries.net (2026). The chart classifies "Institutional/Identified" as the sum of Treasuries, ETFs, and Government holdings. "Retail/Distributed" is calculated as the residual of the Total Circulating Supply.

Antifragility via distribution

Concentration is fragile: when ownership is held by a small number of actors, a single liquidity need can dominate price. Antifragility via distribution describes the evolution toward a market anchored by a broad set of participants - ETFs, advisors, and corporate treasuries. This fragmentation strengthens market resilience: identical sell-side volumes are absorbed across more balance sheets and time horizons, reducing the risk of destabilizing price impact.

The programmatic floor

A distribution phase requires a buyer of last resort. Bitcoin now exhibits a programmatic floor: a non-discretionary institutional bid, most notably ETF rebalancing and rules-based allocation, that absorbs methodical sell-side flows. This floor is model-driven rather than emotional, creating a degree of surface-level price stability even during periods of supply transfer.

The Guardrail: The institutional floor thesis would be challenged if Bitcoin were to experience net ETF outflows exceeding historical norms during a conventional 20% market correction. If institutional capital exits at the first sign of stress, the implied floor is illusory, and market behaviour remains dominated by short-horizon speculative capital.

BTC vs 10Y real yields: 12-month rolling correlation (Since 2015)

Monthly drift: BTC returns vs 10Y real yield changes

Stablecoin velocity vs. price

Net Stablecoin Issuance acts as the ecosystem's deployable liquidity. Price appreciation unsupported by stablecoin supply expansion reflects a fragile, "Short Squeeze" regime. Durable advances require a new-capital regime, in which rising prices are accompanied by expanding stablecoin balances, indicating incremental buying power rather than forced positioning.

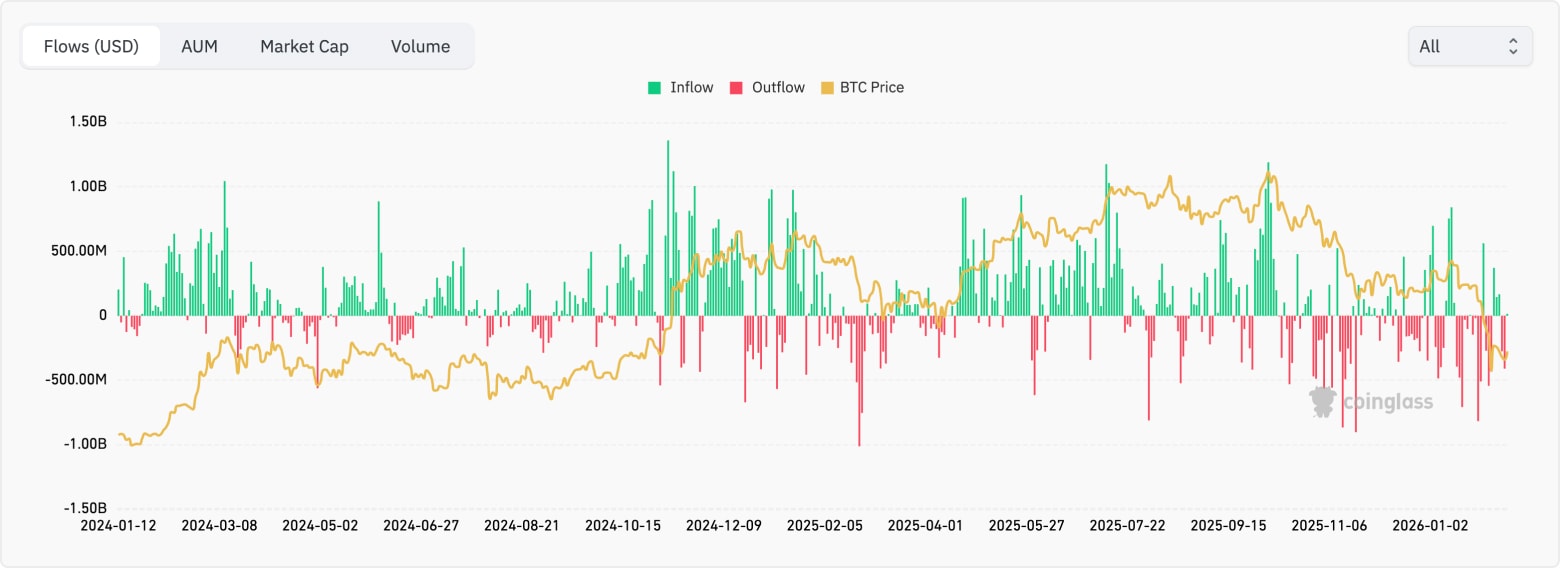

The persistence of ETF flows

The relevance of ETF flows extends beyond daily volume to velocity, consistency, and source. Survey data indicates that advisors allocating to Bitcoin intend to maintain or increase exposure, suggesting a shift from opportunistic allocation to strategic positioning.

This persistence reinforces the view that the current regime is institutional and balance-sheet driven, rather than speculative.

Total Bitcoin Spot ETF Net Inflow (USD)

What allocators get wrong

Institutional perspective: Unbundle the allocation

A common strategic error is treating "crypto" as a single allocation and asset class. Institutional allocators should instead unbundle digital assets into distinct allocation buckets, each with different risk drivers, return profiles, and portfolio roles:

- The "Monetary Reserve" Bucket (Bitcoin): Bitcoin no longer functions as a venture-style bet. It increasingly operates as a macro monetary hedge. Within a portfolio context, it completes with gold and sovereign debt, responding primarily to global liquidity conditions, fiscal credibility, and a long-term debasement risk rather than earnings growth. The objective of this allocation is wealth preservation and diversification, not technological optionality.

- The "Smart Contract Infrastructure" Bucket (e.g., Ethereum, Solana): Smart contract platforms represent digital financial infrastructure rather than monetary assets. Their value is derived from usage, throughput, and fee capture across decentralized applications, tokenized assets, and 24/7 settlement rails. These networks function as the “toll booths” of the future financial system, capturing economic activity through transaction fees and protocol revenues as on-chain finance scales. In portfolio construction, these exposures more closely resemble growth equity or platform software stocks, where returns are tied to adoption and network activity rather than macro hedging properties.

- The "Speculative Alpha" Bucket (Narrative-Driven Assets): This bucket encompasses narrative-driven and early-stage assets - AI-crypto, gaming ecosystems, and emerging Layer 2s - where outcomes are highly uncertain and cyclicality is extreme. These exposures function as venture capital, with success dependent on deep technical diligence, execution risk, and timing rather than macro regime shifts. The goal is asymmetric upside, not portfolio stability.

The question is no longer whether “crypto” is rising or falling. The relevant question is whether each allocation bucket is behaving as expected within its respective regime. Graduation is not measured by momentum, but by the fragmentation of ownership and the transition from speculative positioning to a globally recognized monetary asset.

Collapse

The full breakdown

In our first article, "Navigating Crypto Volatility: The Advantages of Active Management," we explored how the high volatility and low correlation of digital assets with traditional asset classes create unique opportunities for active managers. We discussed how these characteristics enable active managers to execute tactical trading strategies, capitalizing on short-term price movements and market inefficiencies. Building on that foundation, we now turn our attention to the unique market microstructure of digital assets.

Conducive market microstructure of digital assets

The market microstructure of digital assets - a framework that defines how crypto trades are conducted, including order execution, price formation, and market interactions - sets the stage for active management to thrive. This unique ecosystem, characterized by its continuous trading hours, diverse trading venues, and substantial market liquidity, offers several advantages for active management, providing a fertile ground for sophisticated investment strategies.

24/7/365 market access

One of the defining characteristics of digital asset markets is their continuous, round-the-clock operation.

Unlike traditional financial markets that operate within specific hours, cryptocurrency markets are open 24 hours a day, seven days a week, all year round. This continuous trading capability is particularly advantageous for active managers for several reasons:

- Immediate response to market events: Unlike traditional markets that close after regular trading hours, digital asset markets allow managers to react immediately to breaking news or events that could impact asset prices. For instance, if a significant economic policy change occurs over the weekend, managers can adjust their positions in real-time without waiting for markets to open.

- Managing volatility: Continuous trading provides more opportunities to capitalize on price movements and volatility. Active managers can take advantage of this by implementing strategies such as short-term trading or hedging to mitigate risks and lock in gains whenever market conditions change. For instance, if there’s a sudden drop in the price of Bitcoin, managers can quickly sell their holdings to minimize losses or buy in to capitalize on the lower prices.

Variety of trading venues

The proliferation and variety of trading venues is another crucial element of the digital asset market structure. The extensive landscape of over 200 centralized exchanges (CEX) and more than 500 decentralized exchanges (DEX) offers a wide array of platforms for cryptocurrency trading. This diversity is beneficial for active managers in several ways:

- Risk management and diversification: By spreading trades across various exchanges, active managers can mitigate counterparty risk associated with any single platform. Additionally, the ability to trade on both CEX and DEX platforms allows managers to diversify their strategies, incorporating different levels of decentralization, regulatory environments, and security features.

- Arbitrage opportunities: Different venues often exhibit price discrepancies, presenting arbitrage opportunities. For example, managers can buy an asset on one exchange at a lower price and sell it on another where the price is higher, thus generating risk-free profits.

- Access to diverse liquidity pools: Multiple trading venues provide access to diverse liquidity pools, ensuring that managers can execute large trades without significantly impacting the market price.

Spot and derivatives markets (Variety of instruments)

The seamless integration of spot and derivatives markets within the digital asset space presents a considerable advantage for active managers. With substantial liquidity in both markets, they can implement sophisticated trading strategies and manage risk more effectively.

For instance, as of August 8 2024, Bitcoin (BTC) boasts a daily spot trading volume of $40.44 billion and an open interest in futures of $27.75 billion. Additionally, derivatives such as futures, options, and perpetual contracts enable managers to hedge positions, leverage trades, and employ complex strategies that can amplify returns.

Overall, the benefits for active managers include:

- Hedging and risk management: Derivatives offer a powerful tool for hedging against unfavorable price movements, enabling more efficient risk management. For instance, a manager holding a substantial amount of Bitcoin in the spot market can use Bitcoin futures contracts to safeguard against potential price drops, thereby enhancing risk control.

- Access to leverage: Managers can use derivatives to leverage their positions, amplifying potential returns while maintaining control over risk exposure. For instance, by employing options, a manager can gain exposure to an underlying asset with only a fraction of the capital needed for a direct spot purchase, thereby enabling more capital-efficient investment strategies.

- Strategic flexibility: By integrating spot and derivatives markets, managers can implement sophisticated strategies designed to capitalize on diverse market conditions. For instance, they may engage in volatility selling, where options are sold to generate income from market volatility, regardless of price direction. Additionally, managers can leverage favorable funding rates in perpetual futures markets to enhance yield generation. Basis trading, another strategy, involves taking offsetting positions in spot and futures markets to profit from price differentials, enabling returns that are independent of market movements.

Exploiting market inefficiencies

Digital asset markets, being relatively nascent, are less efficient compared to traditional financial markets. These inefficiencies arise from various factors, including regulatory differences, market segmentation, and varying levels of market maturity. For example:

- Pricing anomalies: Phenomena like the "Kimchi premium," where cryptocurrency prices in South Korea trade at a premium compared to other markets, create arbitrage opportunities. Managers can exploit these by buying assets in one market and selling them in another at a higher price.

- Exploiting mispricings: Active managers can identify and capitalize on mispricings caused by market inefficiencies, using strategies such as statistical arbitrage and mean reversion.

The unique aspects of the digital asset market structure create an exceptionally conducive environment for active management. Continuous trading hours and diverse venues provide the flexibility to react quickly to market changes, ensuring timely execution of trades. The availability of both spot and derivatives markets supports a wide range of sophisticated trading strategies, from hedging to leveraging positions. Market inefficiencies and pricing anomalies offer numerous opportunities for generating alpha, making active management particularly effective in the digital asset space. Furthermore, the ability to hedge and manage risk through derivatives, along with exploiting uncorrelated performance, enhances portfolio resilience and stability.

In our next article, we'll delve into the various techniques active managers employ in the digital asset markets, showcasing real-world use cases.

Read full disclaimer