The quality of returns| AI generated image by XBTO

The quality of returns | AI generated image by XBTO

As institutional capital reshapes the market, the conversation is shifting from raw performance to risk-adjusted persistence, and from “how much” was earned to “how well” it was earned. The new measures of success are not just returns and volatility, but endurance, consistency, and control.

This month’s edition of The WIRE explores what defines quality in returns and how traditional portfolio discipline is converging with digital assets. We unpack the metrics that matter, from volatility and drawdowns to Sortino and Calmar ratios, and show how they separate speculative outcomes from sustainable performance. Using XBTO’s Trend strategy as a case study, we illustrate how active management can transform crypto’s raw volatility into smoother, more efficient compounding.

In the end, what matters most is perspective. Returns are the outcome, but risk is the story: the path that determines whether investors can stay the course long enough to see those results realized. True investing skill lies in efficiency: earning returns that are explainable, repeatable, and resilient across cycles.

For a deeper dive, download XBTO’s latest research report: The Quality of Returns - A Practical Guide to Understanding Risk Metrics in Investing.

Why returns alone do not tell the full story

Investing has never been about returns alone. The path taken to achieve them (e.g., the volatility endured, the drawdowns absorbed, and the control exercised along the way) defines whether those returns can be sustained. Traditional investors have long understood this. Over decades, a vocabulary of risk metrics has been developed to describe not just outcomes, but the journey behind them: volatility, drawdowns, Sharpe ratios, downside deviation, and more.

Yet in digital assets, that discipline has often been overlooked. Performance discussions still revolve around price charts and percentage gains, rather than the efficiency or resilience of the strategies that produced them. The result is a narrow, sometimes myopic view of success; one that rewards outcomes without considering what it took to get there, or whether the same process can deliver again.

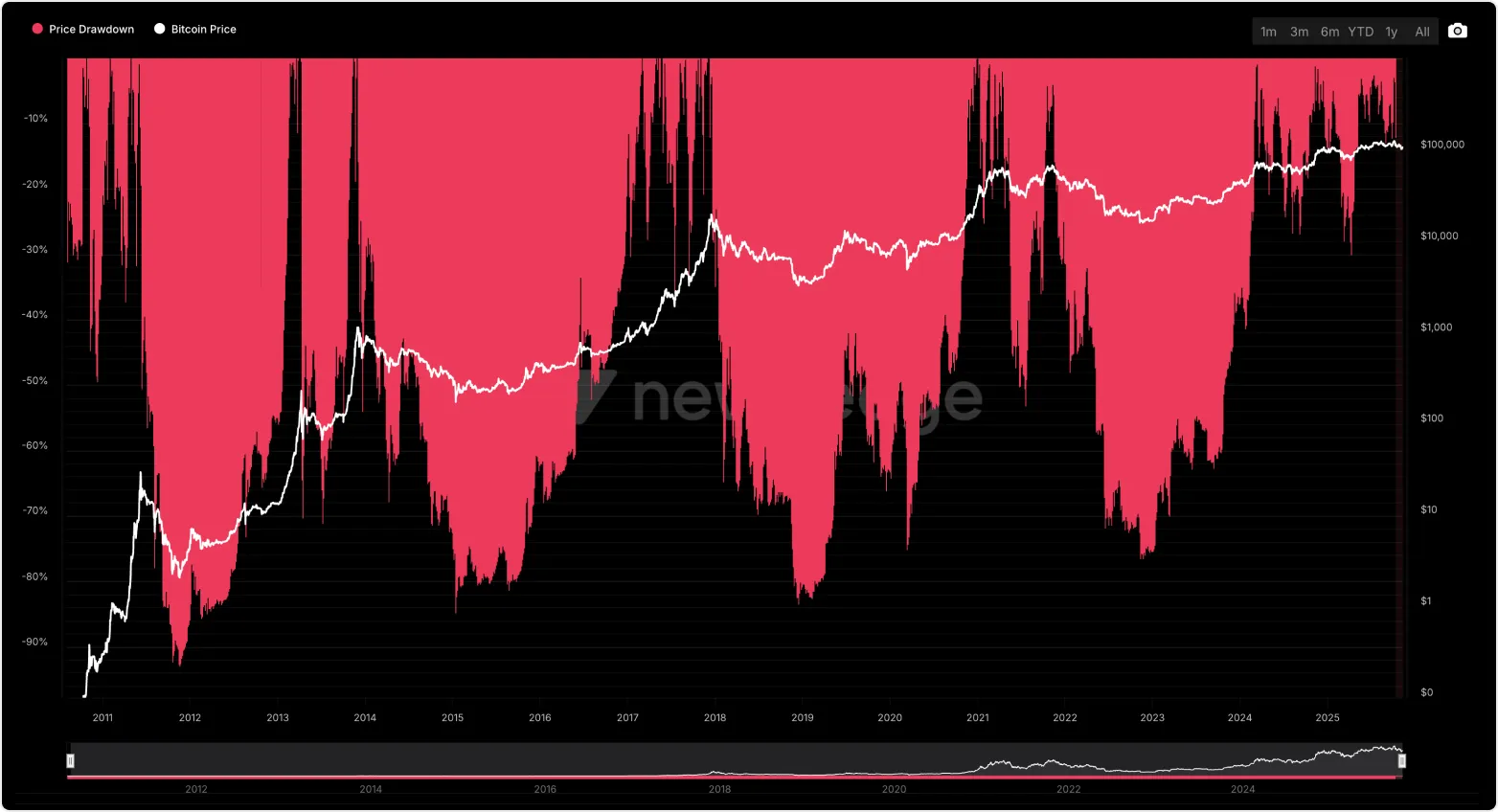

Since 2011, Bitcoin has delivered over 200,000% cumulative returns, yet the path has been defined by deep, recurring drawdowns, including five corrections greater than 70% and more than 400 days spent below prior highs in every major cycle. The chart underscores a critical reality for allocators: exceptional long-term performance has come at the cost of extreme short-term pain. Even as Bitcoin’s price has compounded exponentially, its average drawdown over the past decade exceeds 50%, and volatility remains structurally elevated at roughly 60–70% annualized. Source: Newhedge.

As the asset class matures and institutional capital enters the space, this perspective is changing. The focus is shifting from returns at any cost to returns earned efficiently: those achieved with discipline, consistency, and control. Risk is no longer seen as an unavoidable side effect of opportunity, but as a dimension that can be measured, managed, and ultimately transformed into a source of insight.

These lessons are not new. They come from the history of traditional investing, where understanding risk was never optional but integral to fiduciary responsibility. What is new is their application to digital assets; an industry moving from speculation to strategic allocation, from adrenaline to analysis.

In that evolution, context becomes the differentiator. A 100% annual gain tells us little without knowing how bumpy the road was, or whether investors could realistically stay invested through it. The quality of returns lies not in their magnitude, but in their endurance, i.e., in knowing not just what was achieved, but what was risked to achieve it.

Beyond volatility: The metrics that tell the real story

In our May edition, we argued that volatility isn’t the enemy, it’s the raw material of opportunity. What matters is how it’s managed, not avoided.

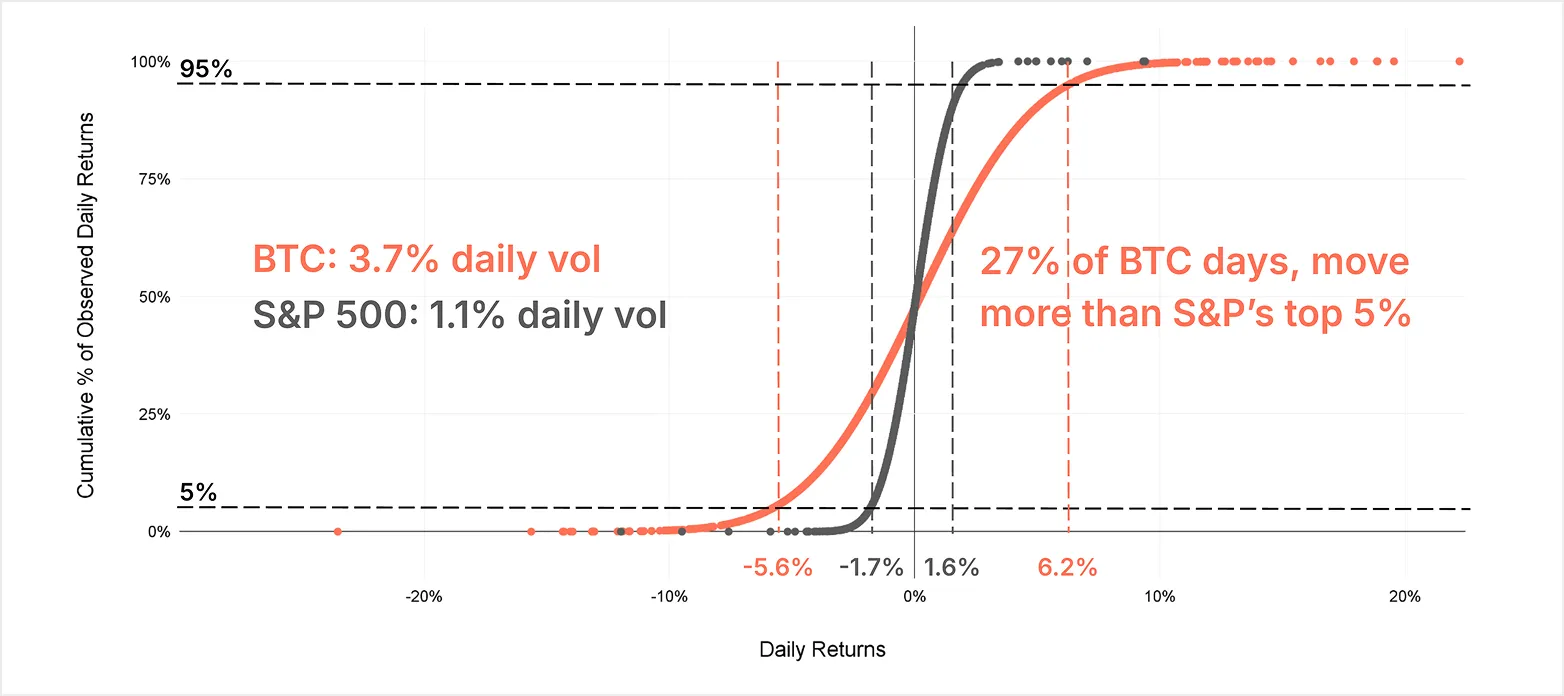

Bitcoin’s return profile reveals consistent tail exposure, in both directions. While traditional assets like the S&P 500 experience rare tail events, Bitcoin operates in a regime where extreme daily moves are routine. With 3.7% daily volatility and 27% of days exceeding the S&P’s 95th percentile, Bitcoin offers both greater risk, and greater opportunity, for those equipped to manage it. This asymmetry underpins its appeal as a source of tactical return, not just directional exposure. Source: GoogleFinance. Period of analysis: 6-May-2016 to 31-Mar-2025.

Volatility has always been part of investing, but in digital assets it often dominates the narrative. Bitcoin’s daily price swings are roughly three times those of the S&P 500; a reminder that in this market, movement itself is constant. But volatility alone doesn’t define risk. It only tells you how much prices move, not towards which direction or what those moves mean.

In traditional investing, decades of experience have turned risk into a measurable discipline. Over time, the industry developed a set of metrics designed to assess not just what was earned, but how efficiently it was earned, and at what cost of uncertainty. Those same tools are now being applied to digital assets, helping investors distinguish speculation from skill. Each metric tells part of the story:

- Volatility measures how turbulent the journey is.

- Downside volatility isolates the pain, i.e., how deep the losses cut.

- Maximum drawdown reveals the worst decline a strategy has had to endure.

- Sharpe and Sortino ratios capture how efficiently risk is converted into return.

- Calmar ratio compares performance to drawdown stress, i.e., how much progress is made for every setback absorbed.

- Shortfall and Expected Shortfall quantify the average and expected size of losing periods, i.e., the “depth of the potholes.”

- Uplift and Expected Uplift mirror those measures on the upside, i.e., the strength and frequency of winning months.

- Beta gauges how much a portfolio moves with the broader market, offering a view of its independence and diversification potential.

Together, these measures convert market noise into meaningful signals, showing investors not just the scale of returns, but the quality of decisions behind them.

In a maturing industry, risk literacy is becoming the new competitive edge.

For a full glossary of metrics, including definitions, interpretations, and intuitive analogies, download the full report.

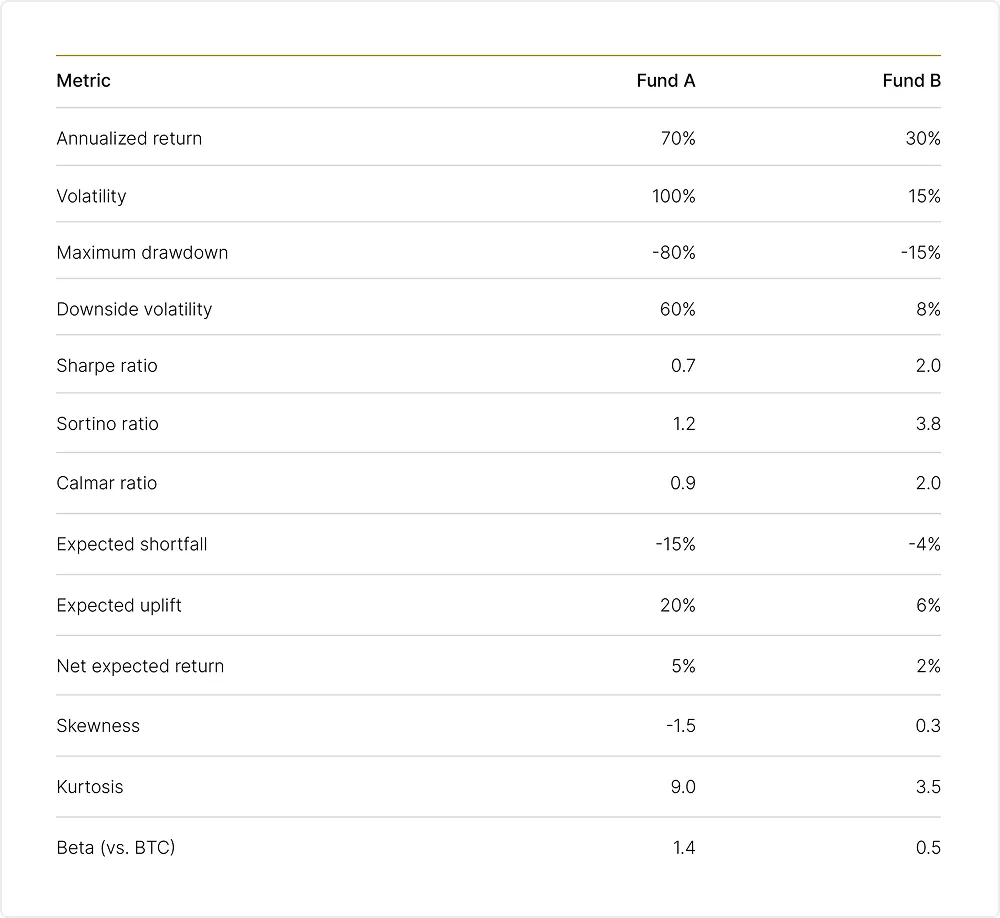

This perspective changes how investors compare funds. Consider the two funds below:

On paper, Fund A’s returns look spectacular (i.e., 70% p.a.), but they came with 100% volatility and drawdowns of 80%. Few investors would endure that ride. Fund B’s 30% annualized return looks modest in comparison, yet it was delivered with steady control: low volatility, shallow drawdowns, and a far smoother path.

The lesson is simple: investors don’t compound returns they can’t hold.

In digital assets, that principle is amplified. A 50% drawdown requires a 100% recovery to break even. An 80% loss demands a 400% rebound. The math of recovery is unforgiving, and it is why allocators focus less on the highest peaks and more on the stability of the climb.

The role of active management

This is where active management earns its keep. XBTO’s Trend strategy illustrates how an active approach can turn raw market volatility into stable, compounding returns.

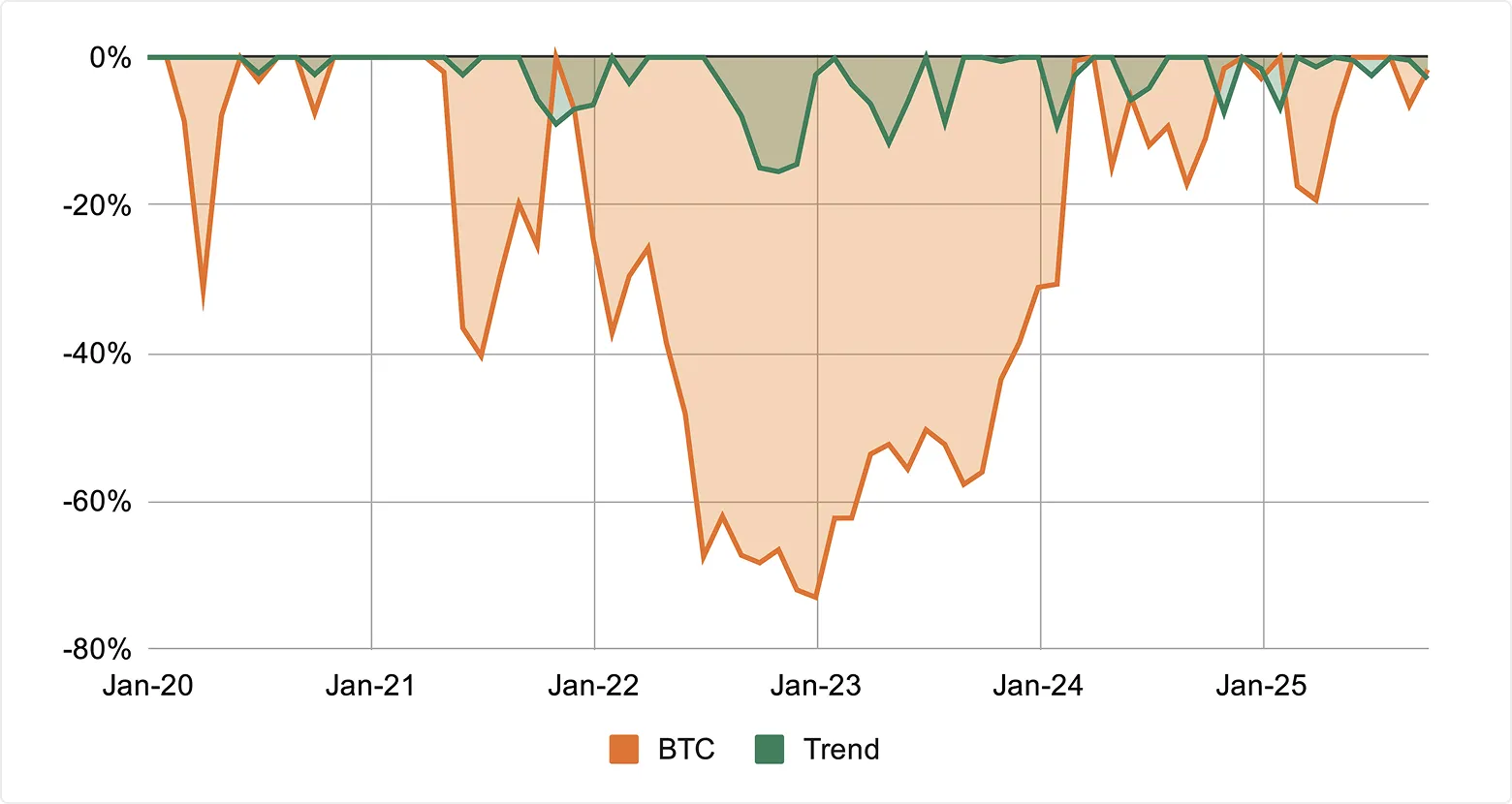

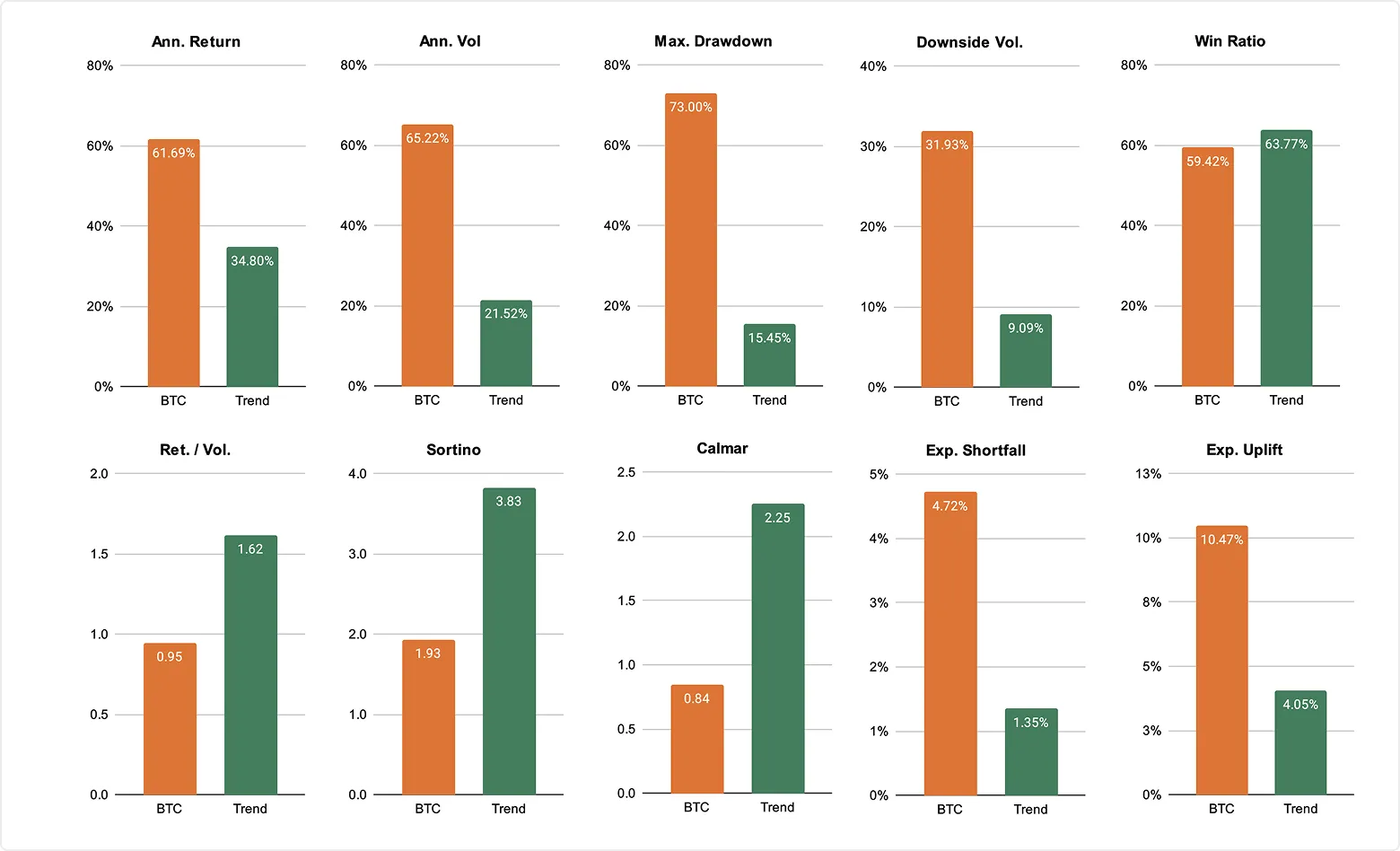

Between January 2020 and September 2025, Bitcoin itself delivered a remarkable 61.7% annualized return, but with 65% volatility, 73% drawdowns, and an expected shortfall of nearly 5% per month. Its path was profitable, but punishing.

Max. drawdown: Active vs. Passive

XBTO Trend, by contrast,captured much of that raw upside while maximizing the efficiency of how it was earned.

Over the same period, Trend produced a 34.8% annualized return with only 21.5% volatility and a 15.5% drawdown. Its Sharpe ratio (1.62), Sortino (3.83), and Calmar (2.25) far surpassed Bitcoin’s.

This isn’t about giving up upside. It’s about transforming uncontrolled movement into managed momentum. Trend’s returns cluster around a modest positive mean, fewer extreme losses, fewer “give-back” months, and a path investors can actually endure.

The result is a shape of return that compounds through control:

- Lower downside volatility and shortfall, limiting capital erosion

- Smaller drawdowns and faster recoveries, preserving compounding

- Higher win rates, consistency, and persistence across market regimes

That’s the essence of active management: not simply chasing peaks, but managing the journey.

Investing in digital assets has entered its next phase - one defined less by speculation and more by structure. With the asset class now exceeding $4 trillion in market capitalization, or roughly 2% of global money circulation, it has become too significant to ignore - and too large to manage without accountability. As institutional participation grows, fiduciary responsibility follows. Allocators are learning the language of digital assets, and crypto managers must now learn to speak the language of investing.

Because in the end, the question that matters - whether in equities, bonds, or digital assets - is the same:

What is the quality of your returns?

Not just how high they rise, but how steady, explainable, and repeatable they are. That’s the standard by which professionalism, and trust, will be measured.

Collapse

The full breakdown

In our first article, "Navigating Crypto Volatility: The Advantages of Active Management," we explored how the high volatility and low correlation of digital assets with traditional asset classes create unique opportunities for active managers. We discussed how these characteristics enable active managers to execute tactical trading strategies, capitalizing on short-term price movements and market inefficiencies. Building on that foundation, we now turn our attention to the unique market microstructure of digital assets.

Conducive market microstructure of digital assets

The market microstructure of digital assets - a framework that defines how crypto trades are conducted, including order execution, price formation, and market interactions - sets the stage for active management to thrive. This unique ecosystem, characterized by its continuous trading hours, diverse trading venues, and substantial market liquidity, offers several advantages for active management, providing a fertile ground for sophisticated investment strategies.

24/7/365 market access

One of the defining characteristics of digital asset markets is their continuous, round-the-clock operation.

Unlike traditional financial markets that operate within specific hours, cryptocurrency markets are open 24 hours a day, seven days a week, all year round. This continuous trading capability is particularly advantageous for active managers for several reasons:

- Immediate response to market events: Unlike traditional markets that close after regular trading hours, digital asset markets allow managers to react immediately to breaking news or events that could impact asset prices. For instance, if a significant economic policy change occurs over the weekend, managers can adjust their positions in real-time without waiting for markets to open.

- Managing volatility: Continuous trading provides more opportunities to capitalize on price movements and volatility. Active managers can take advantage of this by implementing strategies such as short-term trading or hedging to mitigate risks and lock in gains whenever market conditions change. For instance, if there’s a sudden drop in the price of Bitcoin, managers can quickly sell their holdings to minimize losses or buy in to capitalize on the lower prices.

Variety of trading venues

The proliferation and variety of trading venues is another crucial element of the digital asset market structure. The extensive landscape of over 200 centralized exchanges (CEX) and more than 500 decentralized exchanges (DEX) offers a wide array of platforms for cryptocurrency trading. This diversity is beneficial for active managers in several ways:

- Risk management and diversification: By spreading trades across various exchanges, active managers can mitigate counterparty risk associated with any single platform. Additionally, the ability to trade on both CEX and DEX platforms allows managers to diversify their strategies, incorporating different levels of decentralization, regulatory environments, and security features.

- Arbitrage opportunities: Different venues often exhibit price discrepancies, presenting arbitrage opportunities. For example, managers can buy an asset on one exchange at a lower price and sell it on another where the price is higher, thus generating risk-free profits.

- Access to diverse liquidity pools: Multiple trading venues provide access to diverse liquidity pools, ensuring that managers can execute large trades without significantly impacting the market price.

Spot and derivatives markets (Variety of instruments)

The seamless integration of spot and derivatives markets within the digital asset space presents a considerable advantage for active managers. With substantial liquidity in both markets, they can implement sophisticated trading strategies and manage risk more effectively.

For instance, as of August 8 2024, Bitcoin (BTC) boasts a daily spot trading volume of $40.44 billion and an open interest in futures of $27.75 billion. Additionally, derivatives such as futures, options, and perpetual contracts enable managers to hedge positions, leverage trades, and employ complex strategies that can amplify returns.

Overall, the benefits for active managers include:

- Hedging and risk management: Derivatives offer a powerful tool for hedging against unfavorable price movements, enabling more efficient risk management. For instance, a manager holding a substantial amount of Bitcoin in the spot market can use Bitcoin futures contracts to safeguard against potential price drops, thereby enhancing risk control.

- Access to leverage: Managers can use derivatives to leverage their positions, amplifying potential returns while maintaining control over risk exposure. For instance, by employing options, a manager can gain exposure to an underlying asset with only a fraction of the capital needed for a direct spot purchase, thereby enabling more capital-efficient investment strategies.

- Strategic flexibility: By integrating spot and derivatives markets, managers can implement sophisticated strategies designed to capitalize on diverse market conditions. For instance, they may engage in volatility selling, where options are sold to generate income from market volatility, regardless of price direction. Additionally, managers can leverage favorable funding rates in perpetual futures markets to enhance yield generation. Basis trading, another strategy, involves taking offsetting positions in spot and futures markets to profit from price differentials, enabling returns that are independent of market movements.

Exploiting market inefficiencies

Digital asset markets, being relatively nascent, are less efficient compared to traditional financial markets. These inefficiencies arise from various factors, including regulatory differences, market segmentation, and varying levels of market maturity. For example:

- Pricing anomalies: Phenomena like the "Kimchi premium," where cryptocurrency prices in South Korea trade at a premium compared to other markets, create arbitrage opportunities. Managers can exploit these by buying assets in one market and selling them in another at a higher price.

- Exploiting mispricings: Active managers can identify and capitalize on mispricings caused by market inefficiencies, using strategies such as statistical arbitrage and mean reversion.

The unique aspects of the digital asset market structure create an exceptionally conducive environment for active management. Continuous trading hours and diverse venues provide the flexibility to react quickly to market changes, ensuring timely execution of trades. The availability of both spot and derivatives markets supports a wide range of sophisticated trading strategies, from hedging to leveraging positions. Market inefficiencies and pricing anomalies offer numerous opportunities for generating alpha, making active management particularly effective in the digital asset space. Furthermore, the ability to hedge and manage risk through derivatives, along with exploiting uncorrelated performance, enhances portfolio resilience and stability.

In our next article, we'll delve into the various techniques active managers employ in the digital asset markets, showcasing real-world use cases.

Read full disclaimer